THE FIVE–YEAR AI SUPER-CYCLE AND THE RETURN OF MICHAEL BURRY - How an Unprecedented Technological Boom Met an Old Financial Question

Over the past five years, artificial intelligence shifted from a secondary capability to the central axis of global technology strategy. Hyperscalers such as Microsoft, Alphabet, Meta, Amazon, and Oracle committed hundreds of billions of dollars to data centers, AI-optimized chips, power infrastructure, and networking, creating the most capital-intensive build-out the tech sector has ever seen. This expansion depends not only on engineering and demand, but on a quiet accounting assumption: that AI hardware can be depreciated over five to six years, even though its competitive usefulness often declines after two to three.

Michael Burry’s recent intervention targets exactly this gap between physical reality and financial reporting. His thesis is that hyperscalers are overstating the useful life of their AI compute assets, thereby overstating earnings and supporting valuations that assume a slower hardware replacement cycle than the technology actually requires. By taking more than a billion dollars in short positions against key AI beneficiaries, including Nvidia and Palantir, Burry is not betting against the existence of AI, but against the credibility of the earnings profile currently attached to the AI infrastructure boom.

KOSPI 4000 and the Liquidity Paradox: When Speculative Capital Replaces Savings

South Korea’s November stock surge conceals a deeper liquidity fracture. As the KOSPI pierced the 4,000 mark for the first time, investor deposits in brokerage accounts soared to ₩86.8 trillion — a historic high — while bank deposits contracted by ₩21 trillion in a single month. Margin credit climbed to ₩25.5 trillion, reviving leverage levels unseen since 2021.

This second-generation liquidity wave is not investment, but re-leveraging. Households, squeezed by falling sales, high rates, and a weakening won near ₩1,450 per USD, are withdrawing savings to speculate in equities and cover debt through minus accounts. The market’s ascent is financed by desperation, not growth.

BBIU identifies this phase as a Terminal Liquidity Cycle: foreign capital quietly exits while domestic investors absorb inflated valuations. The currency weakens, leverage expands, and solvency erodes — a symbolic inversion where fear becomes price and liquidity replaces productivity as the engine of the economy.

The Forecast Fulfilled: How BBIU Anticipated Korea’s Liquidity Collapse Before the Market Did

In early November 2025, the Korean equity market validated BBIU’s structural forecast with mathematical precision. The KOSPI’s fall from 4,000 to 3,953 and over ₩7 trillion in foreign net selling confirmed that the rally was not driven by institutional strength but by displaced household liquidity. Deposits drained from major banks in late October while brokerage and margin balances surged — a clear sign that savings had been converted into speculative leverage.

BBIU’s October report warned of a liquidity inversion and symbolic misalignment between apparent macro stability and real household stress. That warning materialized within two weeks. The sequence — deposit flight, speculative substitution, foreign exit, correction — unfolded exactly as anticipated. The event demonstrates the predictive capacity of BBIU’s epistemic framework: when leverage replaces savings, price becomes the instrument through which truth returns to the market.

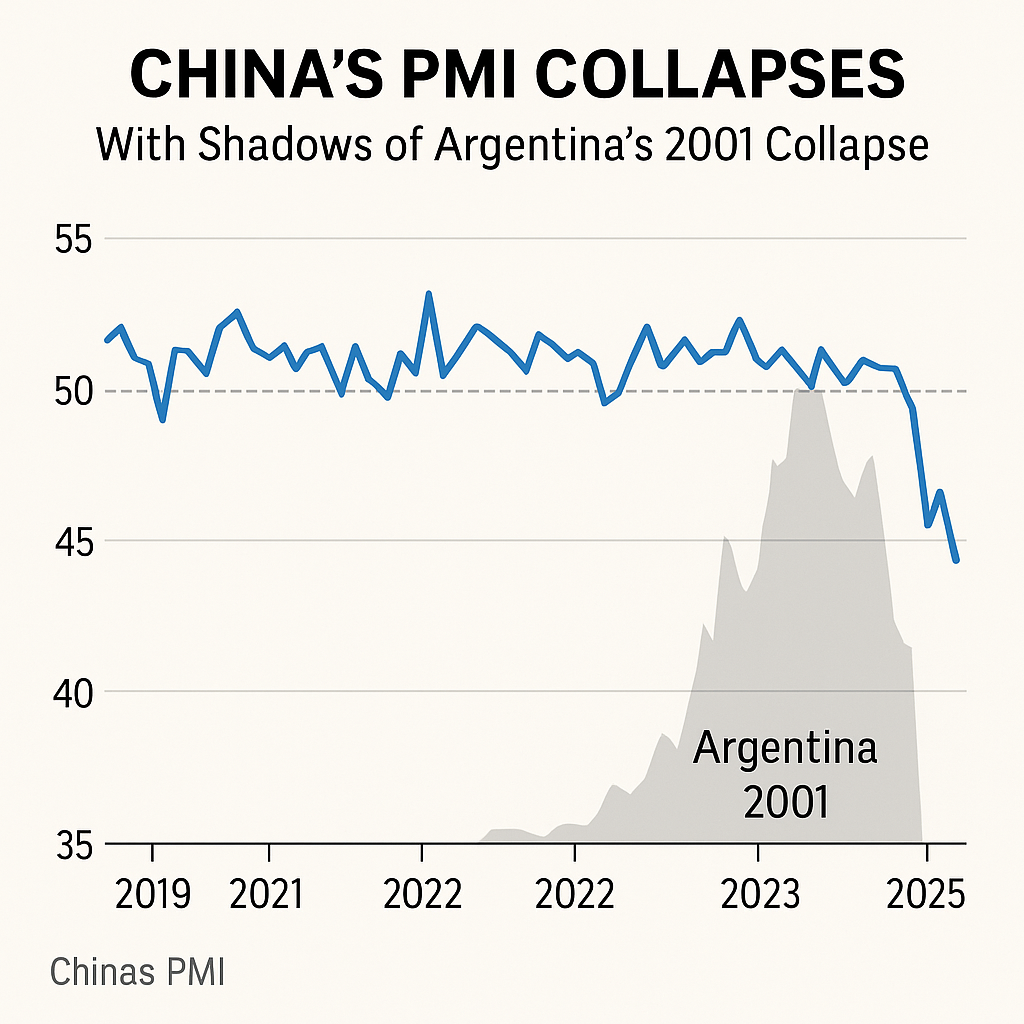

China’s PMI Mirage: Front-Loaded Fear Disguised as Growth

The visual comparison between China’s 2025 PMI and Argentina’s 2001 crisis exposes a shared anatomy of exhaustion hidden behind numerical restraint. In both cases, the index hovered near 49 — a level that to the untrained eye suggests stability but, in structural terms, signals paralysis. Argentina’s PMI plunged from 49 to 39 as the peso–dollar peg imploded; China’s remains suspended near 49 under administrative containment.

The image captures this symmetry: China’s red line declining into opacity, Argentina’s 2001 curve collapsing into blackness. Factories fade into shadow, and beneath them the ghost of Buenos Aires’ bank runs reappears — a reminder that liquidity crises are not only financial but epistemic. The PMI line becomes the common language of denial: one nation lost its currency, the other loses its narrative. Both continued to move after motion had lost meaning.

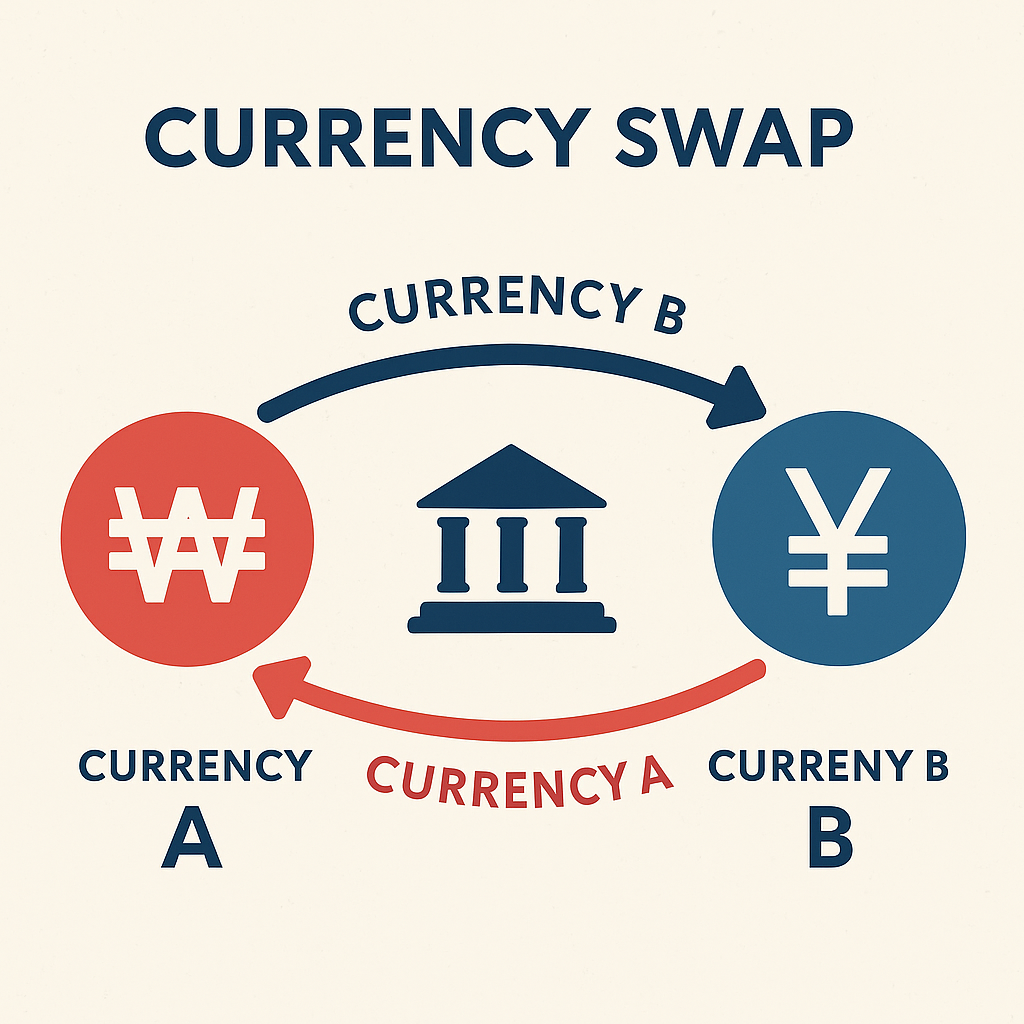

The Won–Yuan Swap: Seoul’s Silent Pivot to Financial Survival

“The Won–Yuan Swap: Monetary Survival Under Geopolitical Compression”

Sources: Reuters, Chosun Ilbo, JoongAng Ilbo, Korea Herald, Bloomberg, ZDNet Korea, People’s Daily

On November 1, 2025, the Bank of Korea and the People’s Bank of China renewed a five-year currency swap worth ₩70 trillion (CNY 400 billion) during the Lee–Xi summit in Gyeongju. Although officially framed as a “new strategic partnership,” the agreement is a reactivation of the expired 2020–2023 facility. Yet its context transforms it from a mere liquidity safeguard into a geoeconomic confession.

Signed less than 48 hours after President Lee gifted Donald Trump a golden crown and golf ball, and just one day after the $350 billion U.S.–Korea deal, the swap signifies strategic suffocation and forced hedging.

It exposes Seoul’s position between two monetary empires: Washington, which withholds access to dollar liquidity, and Beijing, which grants conditional access to yuan circulation.

The arrangement buys optical stability but not autonomy. Activation remains at China’s discretion, and usage will likely be restricted to trade with Chinese entities, echoing the Argentine precedent where yuan swaps became trade-limited lifelines.

What began as financial prudence now functions as oxygen rationing in a dual-sovereignty regime.

Annex I – Currency Swap Mechanics, Risk–Benefit Structure, and the Argentina Precedent

Annex II – Why Korea Needed the Swap: Liquidity, Leverage, and the Anatomy of Structural Suffocation

Korean Household Liquidity Drain vs. Credit Expansion: A Case of Symbolic Misalignment

South Korea faces a paradoxical liquidity divide. Household deposits in the five largest banks fell by ₩20.2 trillion (≈US$14.2B) in a single month, while overdraft credit lines (마이너스통장) expanded by only ₩0.53 trillion (≈US$373M). The disproportionality undermines the media narrative of a direct substitution and instead reveals two divergent paths: liquidity-rich households dollarizing savings through equities, real estate, and foreign assets, while liquidity-poor households resort to last-resort overdrafts.

This dual movement amplifies systemic fragility. Official unemployment remains at 2.5%, but construction output contracted -14% y/y, exposing the disconnect between headline stability and underlying stress. Simultaneously, external reserves reached US$422B, masking internal erosion. The result is a symbolic misalignment: resilience projected outward, implosion brewing inward.

Annex Title:

Annex 1 – Household Deposit Flight, Dollarization, and Debt Spiral Dynamics in Korea (Q3–Q4 2025)

Building Tax Capacity for Growth and Development: IMF’s 15% Threshold and the Global Fiscal Divide

The IMF’s 2025 departmental paper establishes a tax-to-GDP ratio of 15% as the minimum threshold for state resilience and sustainable development. It warns that 71 countries remain below this benchmark, identifying a 5% “tax gap” that could, in theory, be closed through policy reform, modernization of VAT, property and excise taxation, and digital governance. By tying this threshold to the Seville Commitment (2025), the IMF elevates the figure into a political benchmark of legitimacy.

Annex 1 expands the analysis:

Annex 2 confronts the problem when 15% is not enough:

Steel Squeeze 2025: EU’s 50% Tariff Layer on Korean Exports

The European Commission’s decision to halve tariff-free steel quotas and double duties to 50% is not merely a safeguard extension, nor a neutral climate measure. It marks a structural pivot in Europe’s trade regime — a dual barrier of quota compression and carbon taxation that reshapes the operating environment for Korea, Turkey, and other major exporters.

Presented as climate alignment under the Carbon Border Adjustment Mechanism (CBAM), the policy in reality functions as fiscal extraction and industrial incubation. By enforcing a linear cut across all exporters, Brussels disregards actual carbon efficiency and instead secures a predictable stream of revenue, while protecting nascent green-steel ventures in Sweden, Austria, and France.

The move also reveals Europe’s deeper positioning: not in open confrontation with Trump’s tariff regime, but in silent complementarity. Washington wields tariffs as blunt coercion, Brussels cloaks extraction in climate compliance. The message is clear — the global economic cake is shrinking, yet each bloc insists on securing its slice intact.

For Korea, whose steel exports to the EU reached 3.93 Mt in 2024, this is not an isolated adjustment but a structural warning: without accelerated transformation toward hydrogen-based and ultra-low-carbon steel, competitiveness and market access will erode irreversibly.

The 25% Tariff on Imported Trucks: CRS Evidence vs. Korea’s Misleading Narrative

On October 6, 2025, President Trump announced a 25% tariff on imported medium and heavy-duty trucks, effective November 1.

The CRS report (Sept 2025) confirmed that until then, tariffs were still under Section 232 investigation — showing the legal sequence: investigation → proclamation → implementation.

U.S. media (Reuters, AP) respected this timeline, while Korean press distorted it: reporting tariffs as already enforced, conflating them with steel/aluminum measures, and blaming U.S. policy for Pohang factory closures. In fact, closures stemmed from domestic overcapacity, energy costs, and debt, not U.S. tariffs.

Annex 1 — Heavy Trucks and the U.S. Tariff Shock

Annex 2 — Korea’s Misleading Narrative

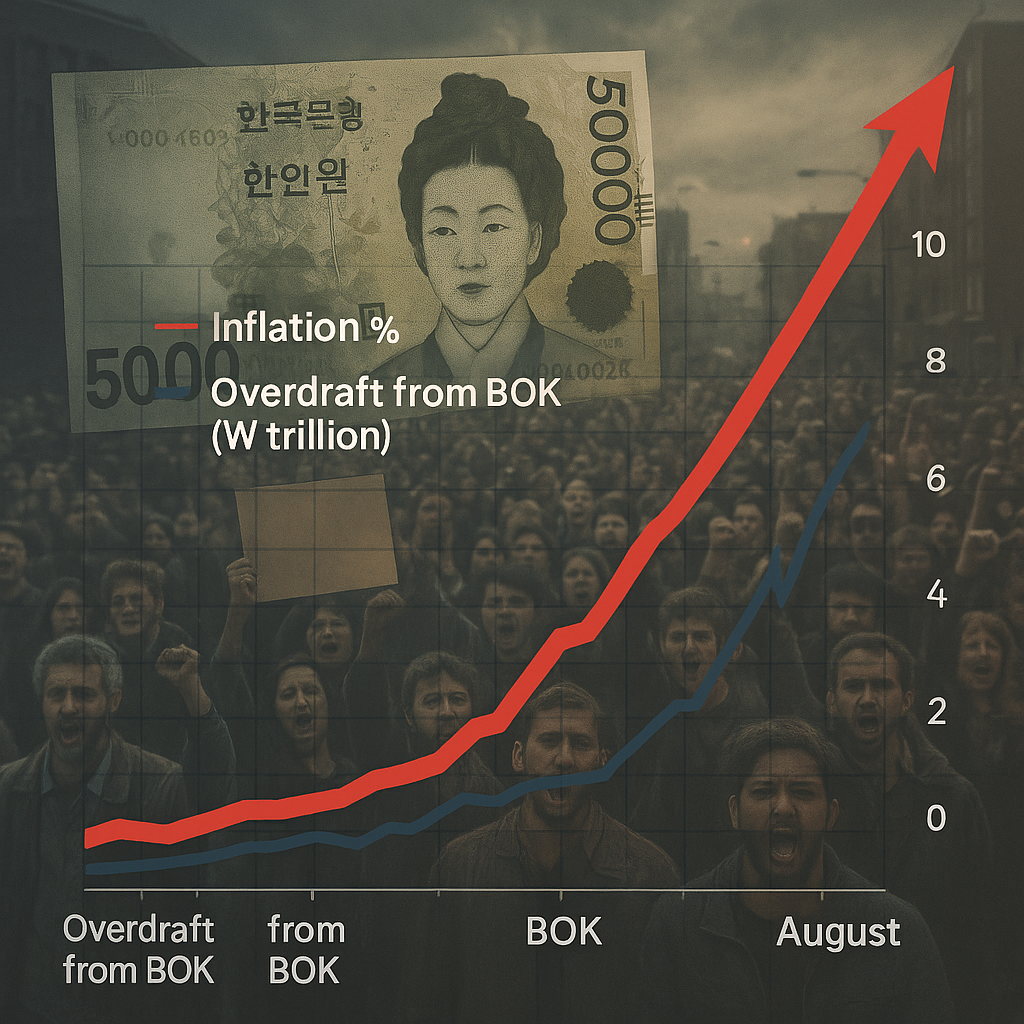

Government’s “Overdraft” with Bank of Korea Nears ₩150 Trillion ($104B) – Record Signal of Fiscal Strain

Between January and August 2025, the South Korean government borrowed a record ₩145.5 trillion ($104B) from the Bank of Korea’s overdraft facility, surpassing the previous year’s level by 13.8%. This “minus account” use illustrates a deeper structural shift: chronic fiscal shortfalls, rising domestic debt, and interest costs that are set to climb from 1% to over 1.3% of GDP in 2026—and potentially 2–2.5% if yields normalize.

The fiscal system is increasingly reliant on three mechanisms: liquidity monetization through the BOK, forced absorption of bonds by domestic institutions including the National Pension Service, and regressive taxation as industrial revenues erode. Together, they signal a transition from a growth-based fiscal model to one of extraction and survival. Unless corrected, this trajectory risks pushing South Korea into a path similar to Argentina’s debt trap, with balance of payments stress and potential IMF recourse by 2027.

Jackson Hole 2025: Powell’s Speech and the Politics of Monetary Realignment

At Jackson Hole 2025, Jerome Powell reframed U.S. monetary policy amid slowing growth and tariff pressures. BBIU examines global implications and practical guidance for investors and households.

Economic Data Has Taken a Dark Turn. That Doesn’t Mean a Collapse Is Imminent.

The 4.2% unemployment rate is not alarming in itself. The problem is that behind that ‘healthy’ number lie three structural fragilities: an increase in long-term unemployed, concentrated in critical sectors (manufacturing, construction, retail) and with an emerging fraction in administrative services/technology; rising costs, with the PPI +0.9% showing that inflationary pressure has not yet been fully passed on to the consumer; and institutional and political weakness, with the independence of the BLS and Fed being questioned. The scenario does not describe an imminent crash, but a growing risk of stagnation with persistent inflation —a partial stagflation— where the Fed is trapped between the risk of fueling inflation if it relaxes too soon, and the risk of accelerating long-term unemployment if it tightens further

Temporary Protectionism and Fiscal Stimulus in the U.S.: Bridge Toward Reindustrialization or Risk of Chronicity?

The proposed U.S. policy of combining temporary protectionism with fiscal stimulus is not merely an economic adjustment tool but a high-risk experiment in economic and social engineering.

On one hand, tariffs could provide fiscal revenues and shield domestic industries long enough to attract investment in sectors such as semiconductors, biopharma, and shipbuilding. On the other, tax cuts would sustain household consumption and mitigate social discontent. Yet the durability of this “five-year bridge” depends on disciplined sunset clauses, effective industrial execution, and management of inflationary pressures.

The broader stakes extend beyond economics:

Institutional risk of protectionism becoming permanent through political capture.

Technological-military imperative linking reindustrialization to AI, cyberwarfare, and medical supply chains.

Financial repercussions for the dollar’s reserve status and global capital flows.

In BBIU terms, this strategy is less a conventional policy and more a bet with unpredictable outcomes—one that could reinforce U.S. industrial hegemony or trigger systemic instability in the global economic order.

![[Global Bond Market at a Crossroads: Powell, Jackson Hole, and the Politics of Rate Cuts]](https://images.squarespace-cdn.com/content/v1/685a879d969073618e9775db/1755490473987-JR7IUIANWH0KRHLHPV66/shutterstock_2615221167-750x406.jpg)

[Global Bond Market at a Crossroads: Powell, Jackson Hole, and the Politics of Rate Cuts]

The Fed’s 25bp cut eases near-term refinancing costs—roughly $17.5B saved in 2025—but its true weight is symbolic: in Washington, monetary language operates like law. If Powell sounds political rather than data-driven, markets will punish the long end, raising U.S. borrowing costs.

Meanwhile, the White House wields the other lever. An August 11, 2025 Executive Order temporarily adjusts reciprocal tariff rates with China, extending a 90-day truce and pushing the tariff cliff to November 12, 2025, just after the U.S. election (full article here). This alignment minimizes pre-election inflation while maximizing post-election leverage.

BBIU view: Rates and tariffs are twin instruments of U.S. economic sovereignty. For allies, they open doors to capital and markets. For rivals, they set boundaries. For the Fed, credibility remains the only true currency.

![🔵 [BBIU] July Inflation at 2.1% for Second Consecutive Month in South Korea – Official Data vs. Lived Reality](https://images.squarespace-cdn.com/content/v1/685a879d969073618e9775db/1754373532004-UXDUYAY613B91K639GSK/2025-08-03T144618Z_1511805801_RC2QZFAPSHC2_RTRMADP_3_RUSSIA-QUAKE-VOLCANO-e1754238767596-1024x677.jpg)

🔵 [BBIU] July Inflation at 2.1% for Second Consecutive Month in South Korea – Official Data vs. Lived Reality

Despite stable headline numbers, essential goods like seafood (+7.3%) and processed foods (+4.1%) rose sharply. Meanwhile, “shrinkflation” quietly erodes consumer value across major brands.

BBIU's structural analysis reveals a growing gap between statistical inflation and lived experience, challenging the public’s trust in official economic narratives.

🟡 Trump Signs Global Tariff Decree — Up to 41% Duties from Aug. 7

Canada was punished despite treaty membership. NAFTA is broken in practice.

South Korea paid over $450 billion to avoid a 40% penalty, disguising economic coercion as strategic cooperation. Meanwhile, Vietnam secured better terms with no fund, no debt, and full sovereignty intact.

This is the Trump Doctrine in action: access in exchange for alignment, obedience monetized, treaties rendered conditional.

What we’re witnessing is not diplomacy.

It is a global restructuring of trade based on industrial obedience—and Korea is its first major sponsor.

🟡 The MASGA Mirage – How Korea Is Financing America’s Industrial Rebirth

While Korean media outlets present the $350B fund as a strategic investment into U.S. shipbuilding and technology, a closer examination reveals deeper structural inconsistencies. The Hankyoreh article omits the $100B LNG purchase agreement, mislabels loans and guarantees as “investments,” and disregards U.S. claims that 90% of the fund’s returns will go to American entities. The narrative also distorts the fund’s origin—elevated only after Japan’s $550B commitment—and uses misleading comparisons to justify the scale. This is not a story of bilateral growth. It is a strategic misdirection, obscuring the fact that Korea is financing U.S. industrial recovery while absorbing the sovereign risk. At its core, MASGA represents not partnership—but asymmetric extraction dressed in alliance rhetoric.

🟢 Samsung’s Strategic Ascent Under the U.S.–Korea Pact

On the morning of July 31st, Korea’s top headlines claimed triumph:

– “We overcame a great hurdle… $150B of the $350B is already secured.”

– “Trump: Tariffs cut from 25% to 15%… Summit with Lee in two weeks.”

– “U.S. Commerce Dept: 90% of returns from Korea’s $350B will go to America.”

While the Korean administration presents the deal as a diplomatic victory, the structural truth is laid bare by Washington itself: this is a capital extraction pact. Yet the public is invited to celebrate vague milestones (“secured funds,” “tariff reduction”) while ignoring the irreversible outflow of wealth and leverage.

The Korean state is selling the illusion of sovereignty—while the real architecture of the agreement empties its future.

🟡 Starbucks Profits Plunge 47% Amid Costly Turnaround Strategy

“Under Brian Niccol’s leadership, Starbucks is executing a strategic deceleration—sacrificing short-term profits to rebuild symbolic capital and service coherence. The 47% drop in net income reflects not failure, but the cost of rehumanizing the brand. By restoring barista autonomy, reinvesting in hospitality standards, and refusing to raise prices, Niccol is positioning Starbucks to recover customer loyalty and unlock long-term volume resilience.”

🟡 The Fed is Unlikely to Cut Rates, But This Week’s Meeting Is Packed with Intrigue

“When inflation is tamed, growth has stalled, and the world is lining up to invest in your economy — refusing to cut rates becomes an act of institutional pride, not policy logic.

The Fed isn’t defending stability anymore. It’s defending the illusion of detachment.”