The White House Blow-Up: Why Trump’s Disphonic Outburst Points to South Korea as the Target of His Trade Fury

Five days ago, at the White House, Donald Trump delivered a press briefing where he appeared visibly exhausted and spoke with a strained, almost broken voice. Half in jest and half in warning, he said he had lost his voice “screaming at people who were stupid” about a trade deal already agreed to — but now being renegotiated. While early speculation pointed toward Australia or Canada, BBIU’s structural analysis shows that only South Korea fits every detail of the timeline, conditions, and symbolic context.

In Trump’s worldview, a verbal commitment spoken on U.S. soil — the $350B investment pledge announced publicly by President Lee on July 30 — constitutes a binding contract. In Seoul’s political culture, however, spoken commitments are provisional and renegotiable. This mismatch transformed diplomacy into punishment. Korea believed that delaying would weaken pressure; instead, Trump weaponized time. His recent remark about being “tired of what happened in Georgia” was not about immigration enforcement — it was a declaration that the grace period has expired. The confrontation has now shifted from negotiation to symbolic discipline, and Korea is the demonstration case.

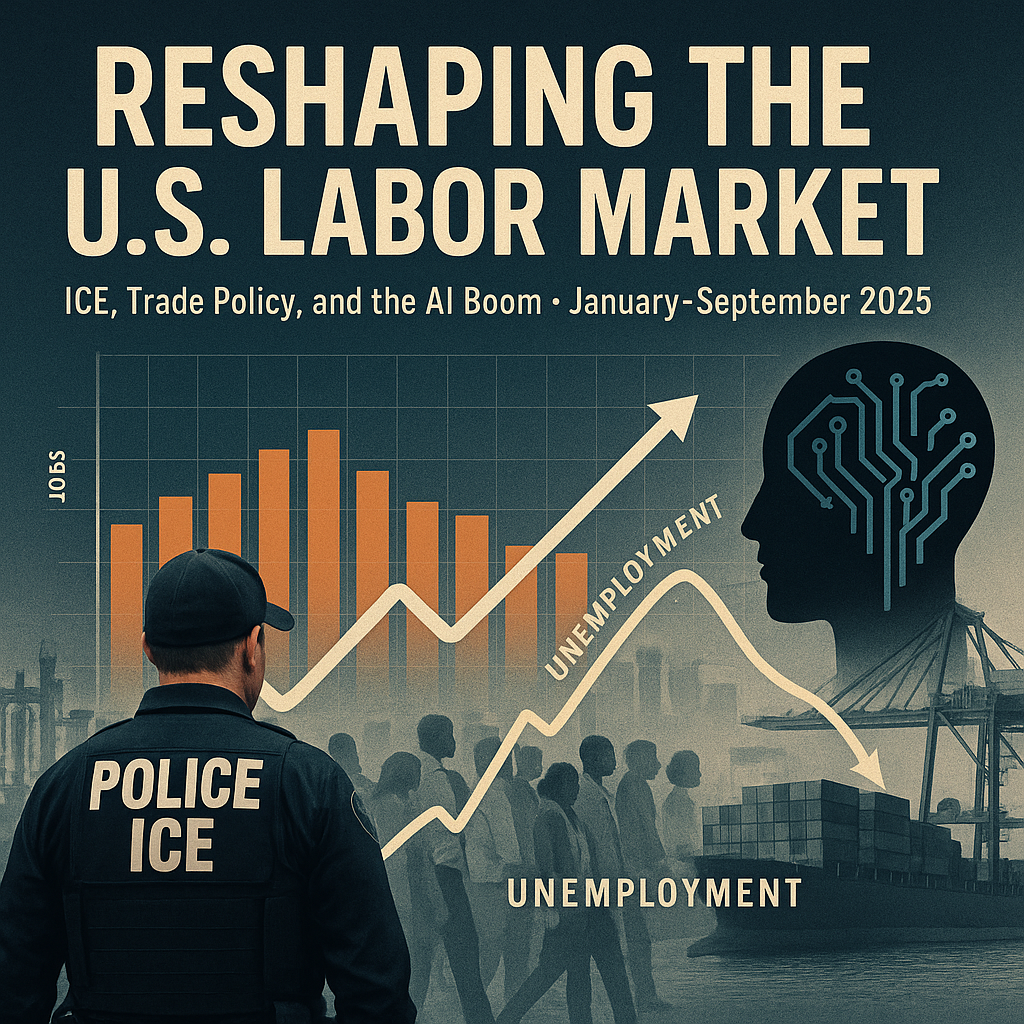

The ICE Shock: How Migrant Enforcement Is Reshaping U.S. Labor Dynamics, Price Structures, and Long-Term Formalization

From January to September 2025, the United States experienced the most profound labor realignment in its recent history. A massive ICE enforcement wave quietly removed more than two million undocumented workers from sectors that had depended on them for decades. At the same time, tariffs reshaped supply chains and the federal government elevated AI to the category of national infrastructure. These forces collided to produce what looked, at first glance, like a contradiction: rising non-farm payrolls alongside rising unemployment. But the pattern was not contradictory—it was the signature of a system being reorganized from the inside. Firms struggled through a short period of disruption, then began replacing invisible labor with formal workers, pushing payrolls up while temporarily elevating unemployment. What emerged was a labor market that is more transparent, more expensive, and structurally more dependent on AI-driven productivity than ever before.

SC | The Real Competitive Frontier: Why Edelman’s 20-Million Theory Is Incomplete, and Why AI Power Depends on User Type, Not Population Size

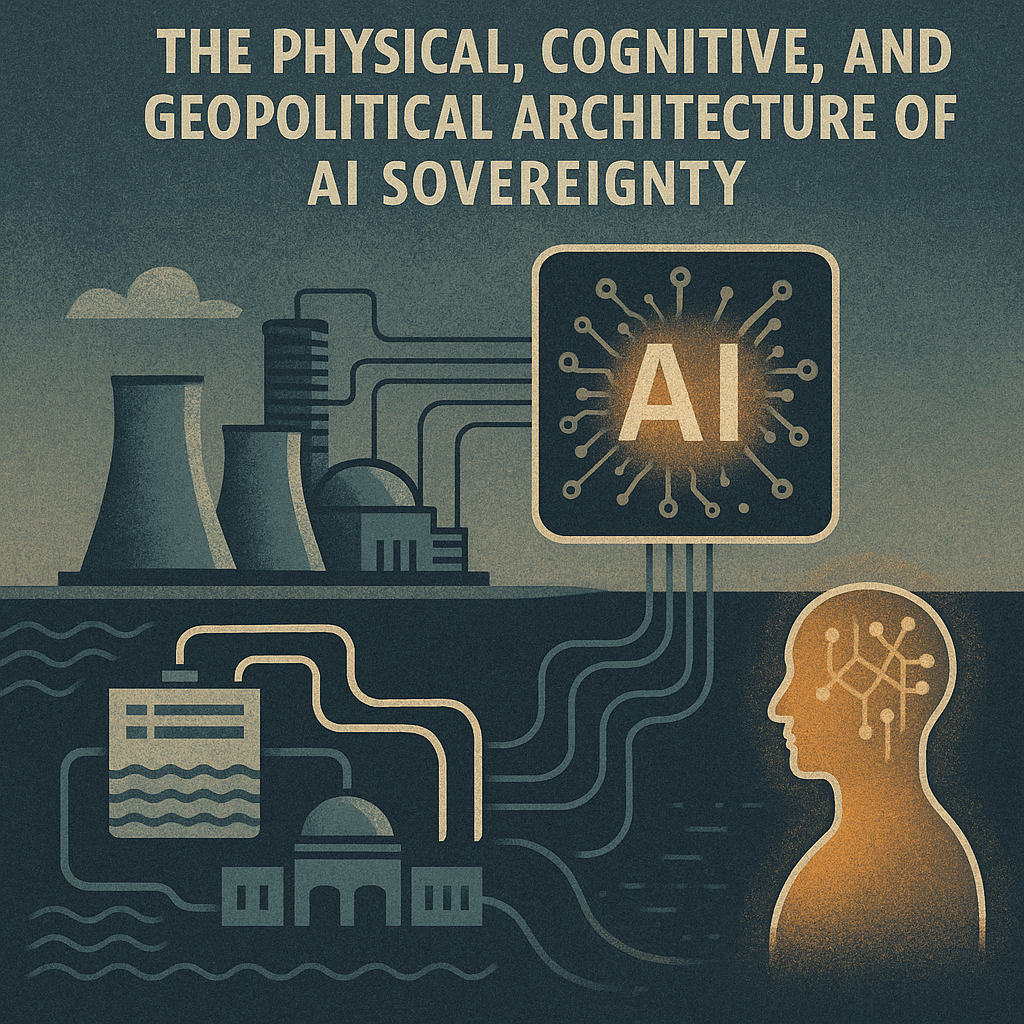

Artificial intelligence does not equalize nations; it stratifies them. The core oversight in Edelman’s statement is the assumption that “20 million people who use AI correctly” exist anywhere. Productivity does not scale with population size but with the density of high-tier cognitive operators—Frontier, Architect-Symbiotic, and Ultra-Frontier users capable of imposing structure, correcting drift, and directing models as strategic instruments. BBIU’s analysis shows that a small nucleus of Ultra-Frontier operators can generate national-level leverage that millions of low-tier users cannot replicate. When combined with sovereign energy, subterranean compute architecture, and nuclear-driven water and cooling loops, this cognitive layer becomes a force multiplier unequaled in previous technological eras.

SK Hynix’s ₩600 Trillion Bet: Korea’s Silent Struggle Against Strategic Extraction

South Korea today is more than a nation-state—it is an active front in a geopolitical contest fought not with missiles, but with capital flows, tariff regimes, semiconductor fabs, and nuclear submarine promises. Under intense U.S. pressure, Korea exports its industrial core—semiconductors, shipbuilding capital, biologics—into American soil, receiving in return conditional market access and politically fragile reassurances. Meanwhile, China seeks to preserve Korea’s appearance of sovereignty while turning it into a functional dependency—a “zombie” state controlled through rare earth leverage and asymmetric economic ties. Japan, for its part, quietly positions itself as the ultimate winner: exporting ultrapure semiconductor materials into U.S. fabs while welcoming the erosion of Korea’s domestic industrial gravity.

The ₩600T Yongin announcement is not a display of confidence—it is a survival maneuver. A rhetorical mirror held up to foreign demands. Korea stands increasingly disassembled into functions: a factory for the U.S., a captive market for China, and a downstream channel for Japan. A battlefield without bullets, defined by the rearrangement of power through contracts, production shifts, and the quiet capture of sovereignty itself.

The Nuclear Illusion: What South Korea Is Not Being Told About the U.S.–Korea Pact

South Korea celebrates a nuclear submarine ‘approval’—but the vessel will be built in the United States, fueled under U.S. legal control, and funded by Korean capital. This is not autonomy; it is a dependency pact dressed as strategic partnership. The real victory is Washington’s: Korea raises its military spending to 3.5% of GDP, injects $150 billion into U.S. shipyards, and imports a platform it cannot build or command alone

Extraction Confirmed: Korea’s Regulatory Concessions Mark the Fulfillment of a U.S.-Engineered Capital Realignment

“South Korea has crossed the threshold from negotiation to submission. What began as a tariff adjustment has now spiraled into a structural recalibration of sovereignty, culminating in the insertion of a ‘U.S. Desk’ into the nation’s agricultural governance. This is not cooperation—it is regulatory annexation. Korea’s food security, environmental protections, and industrial autonomy are now vectors of external control. The silence of July has matured into the erosion of November.”

Korea’s Coming Inflation Wave (2026–2027)

Korea is not experiencing the inflation of this government — it is experiencing the delayed echo of decisions made 18–24 months ago. The real price shock, the one structurally embedded in the ₩100-trillion deficits and the industrial retreat toward the United States, will arrive between late 2026 and mid-2027. And when it does, it will hit a population facing a double blow: rising prices with no wage growth.

With no U.S. dollar swap, a politically conditional China swap, and a collapsing domestic industrial base, Korea enters this period with no independent stabilizer. The future inflation is already in the system; it simply has not fully surfaced yet.

From Coercion to Conditional Compliance: China’s Export-Control Retreat and the U.S.–Allies Strategic Pivot (Oct 9 – Nov 9, 2025)

Between October and November 2025, China attempted to weaponize its dominance over critical materials — and discovered the limits of coercive leverage in a coordinated global system. The one-year suspension of export controls on gallium, germanium, antimony, and rare earths marks not reconciliation but exhaustion: Beijing traded geopolitical pressure for domestic liquidity.

For the United States, the timing was perfect. As the Western holiday purchase cycle accelerated, Washington gained both cheaper imports and a disinflationary narrative. The Xi–Trump truce transformed China’s leverage into a timed concession — a one-year bridge until U.S. and Australian refining capacity reaches scale in late 2026.

The outcome is asymmetrical yet coherent: China preserved liquidity; the United States captured time. What appears as a tactical truce is, in structural terms, the redefinition of economic sovereignty through control of industrial calendars.

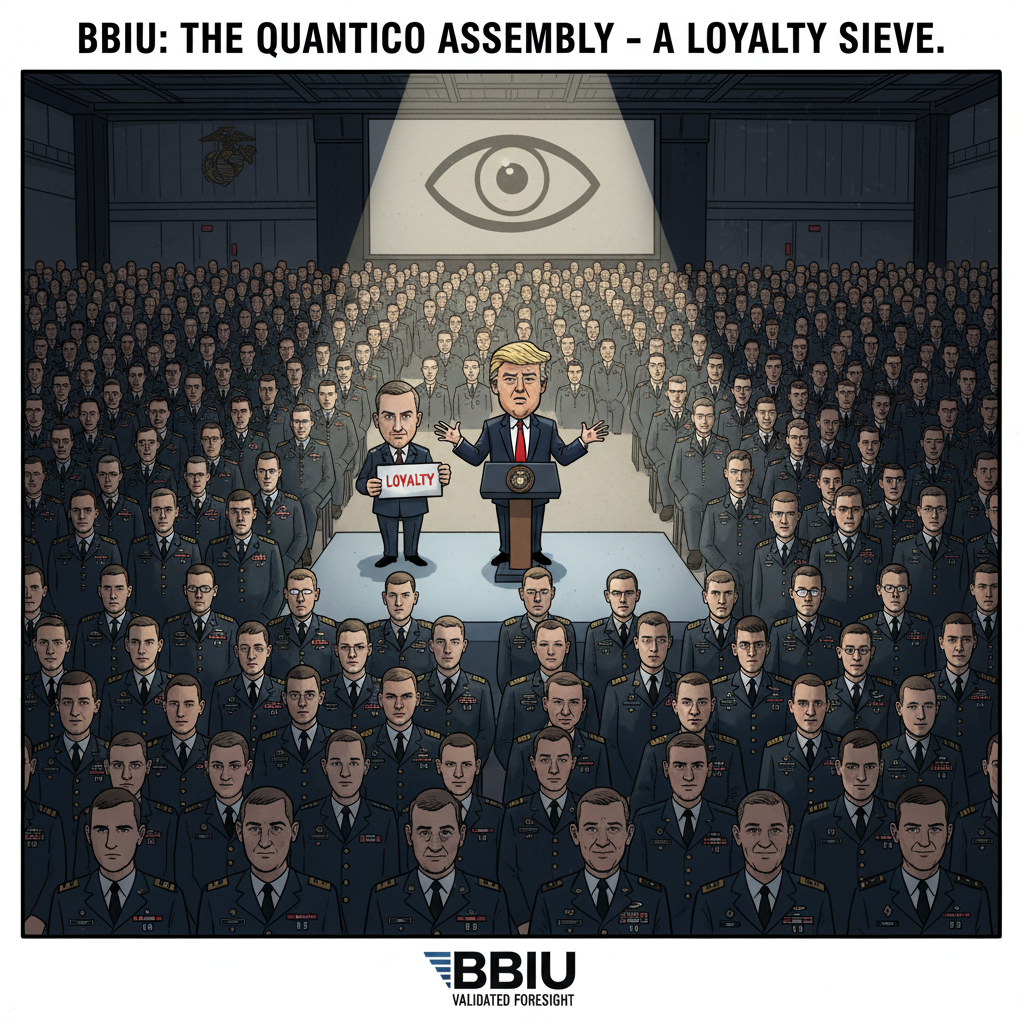

The Quantico Tamiz – How the New York Times Confirmed BBIU’s October Projection

On November 7 2025, The New York Times reported that Defense Secretary Pete Hegseth had “fired or sidelined at least two dozen generals and admirals over the past nine months.”

This revelation confirms what BBIU projected more than a month earlier, in its October 3 analysis “The Quantico Assembly: Trump’s Silent Tamiz of the U.S. Generals.”

What mainstream media now describes as a “purge” was identified by BBIU in advance as a filtration mechanism — a deliberate, data-driven process of ideological alignment within the U.S. military command.

The subsequent removal of roughly twenty senior officers validates BBIU’s structural forecast that the September 30 Quantico meeting marked the beginning of a controlled reconfiguration of military power under the Trump-Hegseth axis.

BBIU’s foresight is now independently confirmed: Quantico was not a motivational gathering, but the first stage of an institutional purge disguised as reform.

The Xi–Trump Summit: Tactical Truce, Structural Submission

The Busan summit between Donald Trump and Xi Jinping marked a temporary stabilization in U.S.–China relations but confirmed a deeper asymmetry in power and intent.

Under the appearance of cooperation, Washington achieved three objectives: regaining agricultural leverage, securing rare-earth supply for one year, and preserving full control over semiconductor restrictions.

Beijing, constrained by deflation, youth unemployment, and capital flight, accepted the truce as a survival measure rather than a strategy.

The one-year duration of the rare-earth clause synchronizes perfectly with the U.S.–Australia industrial corridor’s completion, allowing Washington to reassert dominance once independence is achieved.

Technological containment remains untouched; economic relief is symbolic.

Busan, therefore, was not diplomacy—it was orchestration: a handshake masking a hierarchy, a truce that encodes submission.

Annex A – Technical and Industrial Evidence: Semiconductor Controls and the ASML Incident

Annex B – The Rare-Earth Corridor and the Ten-Point Tariff Illusion

Annex C – Internal China: The Causes and Conditions Behind the Busan Concession

Nuclear Submarines for South Korea: Strategic Authorization or Symbolic Extraction?

On October 29, 2025, Donald Trump announced that the United States authorizes South Korea to construct a nuclear-powered submarine. The approval was framed as part of a larger economic package: tariff reduction from twenty-five to fifteen percent, mandatory purchases of U.S. liquefied natural gas, and a South Korean investment commitment of three hundred and fifty billion dollars. President Lee Jae-myung emphasized that Seoul does not seek nuclear-armed submarines, but conventionally armed vessels powered by nuclear propulsion.

The announcement breaks a long-standing U.S. taboo on transferring naval nuclear technology to non-nuclear-weapon states. For South Korea, the appeal lies in valorizing its vast stockpile of spent fuel, reducing dependence on imported uranium rods, and projecting parity against a nuclear-armed North. For the United States, the core logic is industrial: anchoring construction in Philadelphia, ensuring jobs and contracts for its defense–industrial base, and maintaining full control over nuclear fuel supply.

The symbolism is immediate. China sees another encirclement move, North Korea a justification to expand its arsenal. Seoul gains the image of autonomy, but without enrichment or reprocessing rights, the submarine’s heart remains chained to American supply lines.

Annex 1 — HEU vs. LEU: Definitions and Technical Comparison

Annex 2 — Country Case Examples: How HEU and LEU Are Used in Practice

Annex 3 — International Control Framework: NPT, IAEA, and Bilateral Agreements

ASEAN as the New Factory of the World: U.S. Trade Leverage, China’s Erosion, and India’s Missed Turn

The United States is deliberately reconfiguring its trade architecture in Southeast Asia to reduce dependency on China. The new reciprocal agreements with Cambodia and Malaysia—featuring 0% tariff lanes for key products in food, clothing, and shelter—signal not only an economic shift but also a geopolitical realignment. By opening its market to ASEAN agricultural goods, textiles, and housing materials, Washington simultaneously strengthens domestic inflation control and erodes China’s role as the region’s economic anchor.

China, facing internal debt pressures and declining competitiveness in labor-intensive manufacturing, is losing both export volumes and its symbolic position as the indispensable intermediary in U.S. supply chains. Meanwhile, ASEAN consolidates its role as the pragmatic alternative: feeding U.S. households with rice, palm oil, and seafood; clothing American consumers through relocated textile industries; and supplying construction inputs for U.S. housing. This pivot represents a structural rebalancing of global trade with direct impact on CPI, employment patterns, and geopolitical leverage.

Annex Titles

Annex 1 – GDP Profiles and Product Flows under the 0% Tariff Agreement with the United States

Annex 2 – The Real-Economy Impact on China of U.S.–ASEAN 0% Tariff Agreements

Argentina’s 2025 Midterm Elections: A New Balance of Power in Congress

Argentina’s 2025 legislative elections reshaped the political map in ways both predictable and paradoxical. At the provincial level, La Libertad Avanza (LLA) underperformed: entrenched Peronist machines in the North and Radical strongholds in the Center-West retained control, leaving Milei’s movement with little territorial infrastructure. The consensus was grim—without governors, legislatures, or mayors, LLA seemed destined to remain electorally disruptive but institutionally weak.

Yet the national results told a different story. With more than 40% of the vote, LLA became the largest bloc in the Chamber of Deputies, edging Fuerza Patria in Buenos Aires and prevailing in Córdoba, Mendoza, and Santa Fe. The new Congress, seated in December, now counts 112 seats for LLA, 104 for Kirchnerism, 32 for Juntos por el Cambio, and 9 for provincial forces. The Senate renewal further weakened the opposition, making impeachment threats symbolic rather than realistic. Kirchnerism retains discursive power but lacks the numbers to destabilize Milei institutionally.

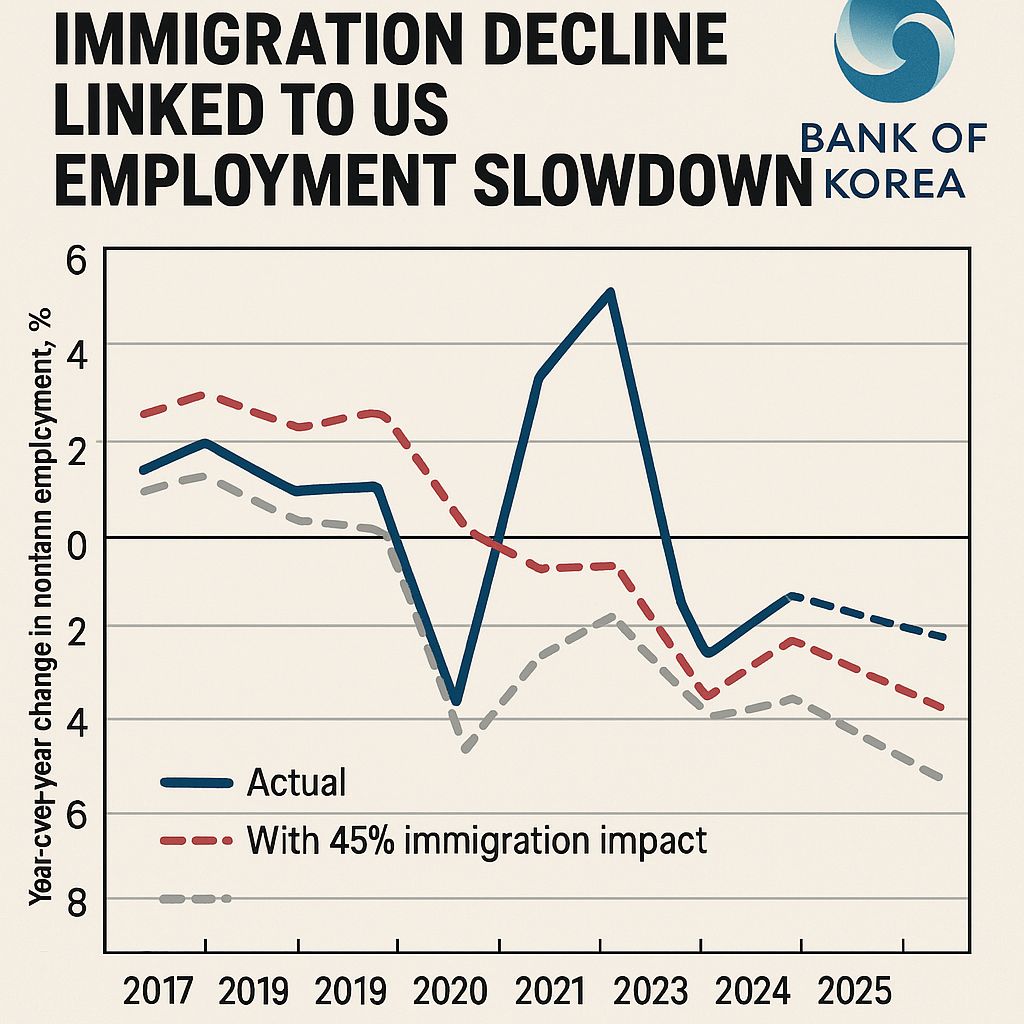

Immigration as Narrative: The Bank of Korea’s Framing of U.S. Labor Slowdown

The Bank of Korea’s latest report attributes nearly half of the U.S. employment slowdown to reduced immigration—a figure not corroborated by any U.S. institution. While the Federal Reserve and other agencies acknowledge immigration as a supply factor, none assign it a precise numerical weight. This selective quantification reveals less about the U.S. labor market than about Korea’s own domestic narrative: immigration is being reframed as an economic necessity, even when the underlying data does not support such certainty.

Annexes

Annex 1 — South Korea: Employment, Immigration, and Crime Nexus (2019–2025)

Annex 2 — Worst-Case Scenario for Korea’s Legislative Elections

India’s Russian Oil Dilemma: Between Trump’s Tariff Pressure and Moscow’s War Revenues

This report examines the structural tension between India’s energy security and U.S. geopolitical pressure, situating Modi’s balancing act within the broader framework of trade, military dependency, and great-power diplomacy. Beyond the Five Laws analysis, the study includes detailed annexes covering the economic and geopolitical foundations of India’s continued reliance on Russian energy.

Annex 1 — Historical Price Variations and Strategic Incentives (2020–2025)

Annex 2 — Geopolitical Drivers of India’s Energy and Defense Policy

Annex 3 — The Korean Defense Channel: Indirect U.S. Armament for India

U.S.–Australia Critical Minerals Deal: Strategic Pivot to Break China’s Grip

On October 20, 2025, the United States and Australia signed a landmark framework to secure critical minerals and rare earths, directly countering China’s tightening export controls. The agreement commits over US$3 billion in near-term investment, positioning Australia as a strategic “friend-shore” supplier and eroding Beijing’s perception of monopoly.

BBIU analysis underscores that China’s dominance is less geological than political—sustained by subsidies, ecological externalities, and coercive policy tools. Without subsidies, “Made in China” loses its artificial cost edge, and price parity emerges for Australia, the U.S., and allied producers. The pact marks the first decisive inversion of leverage: rare earths have shifted from commodity to strategic-security asset.

Annex 1 – Rare Earths: Strategic Dimensions for the Semiconductor Industry

Annex 2 – Strategic Implications for China, U.S., Australia, Japan, and South Korea

Scenario 1 – Prolonged Attrition: Weakening Without Break (with criminal economy variable)

Scenario 2 – Regime Breakdown (CCP Collapse within 24 months)

Annex 3 – Policy & Corporate Recommendations (governments, corporates, subsidy variable)

South Korea’s $350 Billion Dilemma: Between IMF Diplomacy and Trump’s “Upfront” Ultimatum

South Korea’s $350B clash with Washington has shifted from economics to symbolism. Deputy PM Koo Yun-cheol admitted the upfront payment is impossible; Trump insists on it as proof of obedience, mirroring Japan’s capitulation. The trajectory—SPC Trap, Tariff Gamble, Silent Resistance, IMF admission—shows Korea trapped between technical reality and political symbolism. The number is not liquidity, but a test of subordination.

Annex I – Key Missteps by South Korea

Annex II – Structural Constraints & Acceptable Narrative

China’s Robotic Frontier: Western Executives Confront the “Dark Factory” Reality

Western executives visiting China return with an uneasy realization: the country is no longer competing on low-cost labor, but on automation at scale. In 2023 alone, China installed more than 276,000 robots—over half of the world’s total—bringing its operational stock above 1.75 million units. Factories in Shanghai and Shenzhen now operate at near “lights-out” levels, where robotic arms assemble vehicles and electronics with minimal human presence.

Yet behind this futuristic façade lies a fractured social reality. While coastal provinces embrace robotics and AI-driven production, millions of workers in the interior still rely on semi-manual assembly, and rural China remains rooted in labor-intensive agriculture. The result is three Chinas living side by side: one in the 19th century, one in the 20th, and one in the 21st. This temporal inequality is as dangerous as it is striking—an industrial triumph masking a deep social fault line.

Trump’s Retaliation Against China’s Rare-Earth Export Controls and Market Shock

China’s MOFCOM Announcement No. 61 tightens rare-earth export controls and extends them extraterritorially to goods with ≥0.1% Chinese REE content. The U.S. counters: an additional 100% tariff on Chinese imports from Nov 1 (and signals controls on “core software”). Markets slide: Dow −1.9%, S&P −2.7%, Nasdaq −3.56%.

Shock mechanism.

Beijing weaponizes critical materials; Washington weaponizes market access and software. The contest shifts from tariff cycles to choke-point warfare.